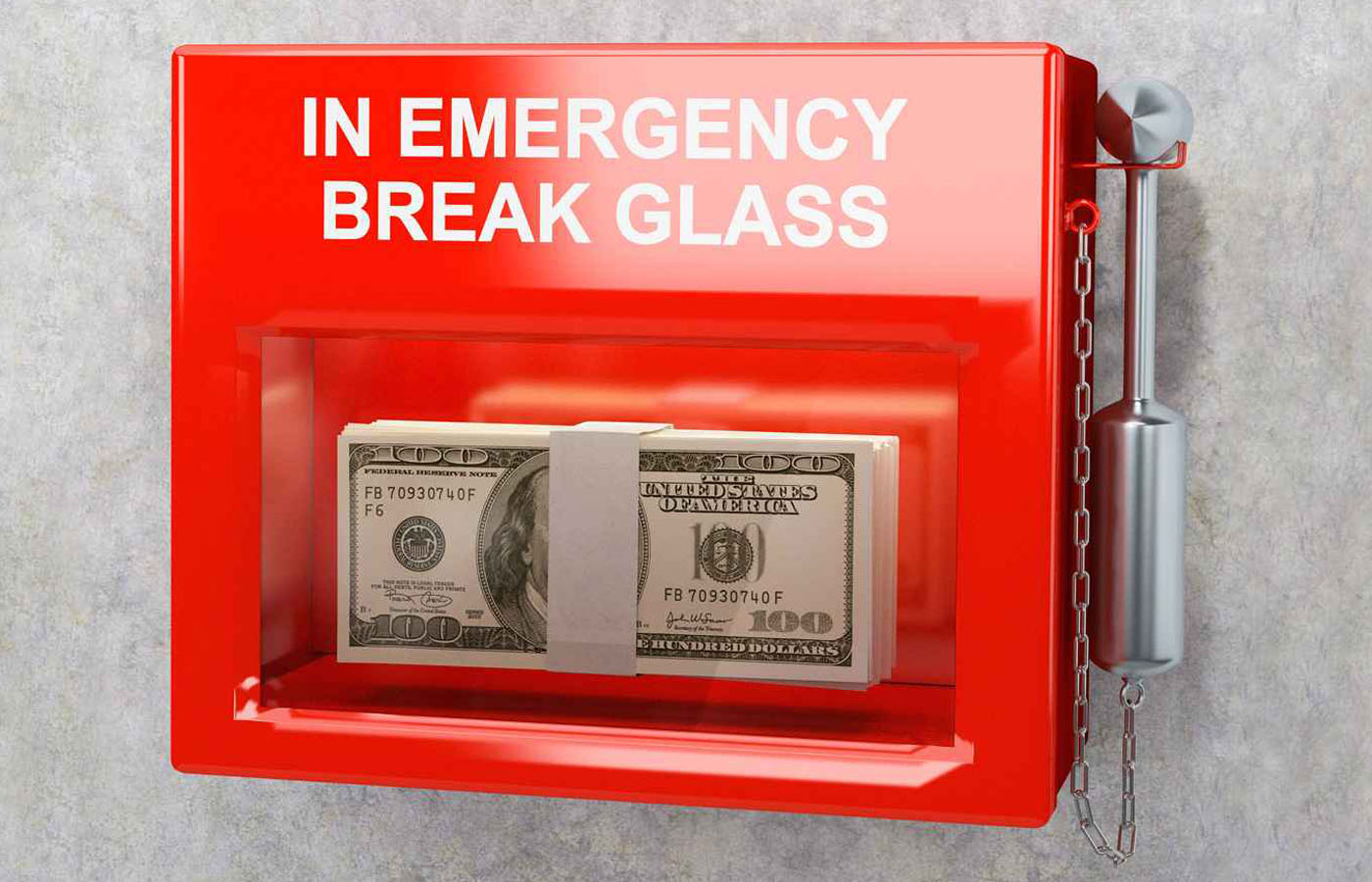

An emergency fund is essential for anyone who is financially independent. Here are 5 rules to help you prepare and emergency fund properly as a safety net should you ever need it. Knowing that enough money is in place will you give you a little peace of mind and breathing room in the event something should happen.

First off, let’s define what exactly is an emergency fund. While it is similar to an emergency safety net, it is a cash cushion that will help protect you from an unexpected financial hardship: job loss, suffering from an accident, or being evicted. You’re aware of those orange life preservers on planes and ships, well, then think of an emergency fund as a “financial” life preserver that will buy you time; most importantly it will keep your head above water and breathing easily should you fall victim to an unforeseen and sudden lull in your life.

A few words, however, to acknowledge the fact that everyone is in a different circumstance with a set of unique financial situations. Some people find themselves with a lot of financial support from their family, others are burdened with student or credit card debt, or both. Any time you read about personal finance tips, work from within your framework and do what’s in your best interest.

Here are five foundational rules for building an emergency fund. When it comes to an emergency fun, you do not want to procrastinate. So don’t delay and get started saving today.

Set a savings goal and work towards it

You need to set a specific goal. Don’t count on yourself stashing away some money here and there without having a nominal goal in mind that is also realistic. Do everything you can to make it a concrete goal: write it down and make it a commitment. When you get close to reaching that goal, you’ll always have the option to raise the bar. Goal setting is an important part of the psychology of the process.

The general rule-of-thumb is still three to six months’ worth of expenses

The gold standard of a mature emergency fund is to have put away enough to cover your expenses for three to six months. To date, this is still a guiding standard for the majority of people out there. It’s possible that you’re someone who would be better off saving for more, like eight to twelve months.

This is where the nuances of your particular financial situation comes into play. If you only have a mortgage, car payment, some bills and groceries to cover, then three to six months’ worth might be enough. But if you’re self-employed or with a disability then perhaps it’s best to go larger.

Keep your emergency fund liquid

Whether you invest your funds or prefer to stuff bills between the mattresses, make sure that the money is liquid. The idea here is to have instant access to the money you’ve worked hard to put away without having to pay additional fees to access it. At the very least, make sure the majority of it remains as cash at hand in a pinch. And if you decide to invest a small portion of it, make sure that it remains low-risk: CDs, Roth IRAs, and savings accounts.

Use a high-interest savings account

Just because the money should stay liquid doesn’t mean that it shouldn’t also be earning interest for you in the interim. Keep in mind that inflation can occur and with it the value of money might fall. Therefore, strive to strike a balance between the value of your dollar and keeping the money accessible. Shop around for savings accounts with the best interest rates (and try to avoid additional fees).

Remember why you started an emergency fund in the first place

Try not to lose focus and forget why you put money away in the first place. Don’t derail your efforts and remind yourself what the funds are designated for. It might be tempting to use that extra cash for a vacation, but resist the urge to splurge – you don’t want to be caught red-handed on an unstable financial footing should things go awry. Be honest with yourself about what an emergency is, and define it. Staying on track involves knowing the goal and sticking to it.

If there are additional things you want to do or need to buy, set aside money in a separate place for those items. Tapping into an emergency fund to cover extraneous items or desires is just plain, not smart.